Practice Update March 2026

Cashflow red flags for small business in 2026

Why 2026 feels tough for many small businesses

If you’re feeling the pressure this year, you’re not alone. Many Australian small businesses are navigating higher interest rates than just a few years ago, rising wages and superannuation obligations, increased insurance premiums, tighter consumer spending, and stronger ATO compliance activity. At the same time, customers are taking longer to pay, while suppliers want their money faster. That squeeze, money coming in slower and going out quicker, is what’s creating real cashflow stress. Even well-run, profitable businesses are feeling it.

Profit is important. Cash is survival. In the current environment of higher interest costs, tighter margins and stronger ATO enforcement, small businesses must actively manage liquidity, not just profitability.

Before we look at real-world scenarios, there are a few important principles every business owner should understand.

Important notes before we begin

- Profit does not equal cash.

Your profit and loss statement shows accounting profit. Your bank account shows reality. - GST, PAYG and super are not your money.

These amounts are collected or withheld on behalf of the government or employees. - Growth consumes cash.

More sales often require more wages, stock and supplier payments before you get paid. - Early action creates options.

Late action limits them.

Now let’s look at common red flags.

Case study 1: Growing sales but shrinking bank balance

Sarah’s Landscaping Business

Sarah invoices $220,000 in one quarter.

However:

- $120,000 remains unpaid at BAS time

- Payroll ($14,000 per week) has already been paid

- Suppliers paid within 14 days

What Happens?

She owes $18,000 GST on invoiced sales, even though much of it hasn’t been collected.

Her bank balance falls below $10,000.

Cashflow Pressure Summary

Lesson

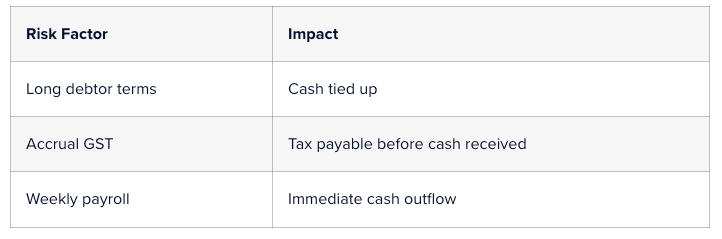

If debtors exceed one month of expenses, you are financing your customers.

Possible actions:

- Request deposits

- Shorten payment terms

- Move to cash accounting (if eligible)

- Tighten collections

Case study 2: The ATO as “silent financier”

Tony’s Café

When margins tighten, Tony delays:

- BAS payments

- PAYG withholding

- Superannuation

After 12 months:

Why is this dangerous

Using the ATO as working capital creates escalating risk:

- Director Penalty Notices

- Garnishee notices

- Denied payment plans if reporting late

ATO debt is rarely the core problem; it’s a symptom.

Lesson

If you cannot pay tax, restructure early:

- Lodge on time

- Enter formal payment plans

- Review pricing

- Reduce fixed overheads

Ignoring tax debt compounds stress.

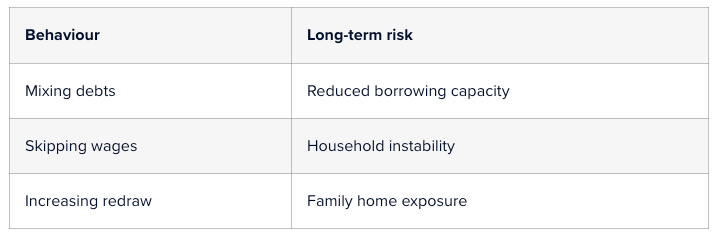

Case study 3: Blurring personal and business finances

Family Retail Business

When business cash dips, the owners:

- Redraw from a home loan

- Use personal cards for stock

- Skip paying themselves

What this creates

The business looks stable. The family balance sheet weakens.

Lesson

Your business must consistently pay you.

If it cannot:

- Review margins

- Reduce stock levels

- Negotiate supplier terms

- Consider downsizing

Your household should not subsidise poor cash discipline.

Case study 4: Growth without working capital

Construction Contractor

Turnover grows from $1.2M to $2.4M in one year.

But:

- Materials purchased upfront

- 60-day payment terms

- 5% retention withheld

Working Capital Impact

James requires an additional $350,000 in working capital, but does not arrange financing.

Suppliers move to cash-on-delivery terms—projects stall.

Lesson

Growth consumes cash before it produces profit.

Before expanding, ask:

“How much extra cash does this growth require?”

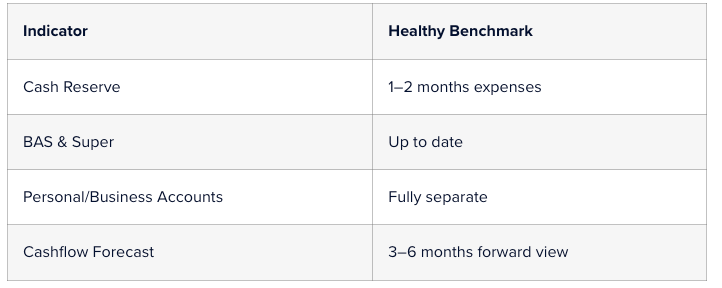

What healthy cash flow looks like

A financially stable business generally has:

Early warning signs checklist

If you recognise two or more of these, act immediately:

- Overdraft is always at the limit

• Unsure of upcoming BAS liability

• Paying super late

• Avoiding ATO mail

• Using credit cards for suppliers

• No clear break-even figure

Cash stress builds quietly, then accelerates.

Final thoughts

Running a small business today isn’t easy. Margins are tighter. Costs are higher. The ATO is more active. And there’s usually a family relying on the business to perform.

The businesses that stay strong aren’t always the biggest or the fastest growing. They’re the ones who know their numbers, plan and act early when something doesn’t feel right.

Profit might look good in a report. But cash is what pays wages. Cash is what covers taxes.

Cash is what helps you sleep at night. If you’re not completely sure where your cash flow stands right now, that’s okay; most business owners are too busy running the business to step back and assess it.

But taking the time to review it properly could be the difference between reacting under pressure and making confident, proactive decisions. And that’s a much better place to be.